What to expect in 2018

An overview of the outlook for global investment markets

Key themes for advisers in 2018

Outsourcing will continue to be a strong theme for financial advisers in 2018, James Rainbow has said.

The co-head of UK intermediary for Schroders said: "We have seen a marked move by financial advisers from building their portfolios to outsourcing some or all of their portfolio management activities."

He said this has been the situation for the past four years and would be likely to continue.

In a video with Eleanor Duncan, deputy content editor for FTAdviser, Mr Rainbow said the direction of that trend to outsource was still varied, with business going to discretionary fund managers, multi-asset, multi-managers and even to ratings agencies who are managing portfolios for advisers.

Mr Rainbow also told FTAdviser that while Brexit was "dominating a lot of conversations between advisers and their clients", he said this was not the primary concern for advisers.

He said: "What an adviser does well for their clients is keep them on the path they have set together.

"What we saw in 2016 when we had the Brexit vote and the US Presidential election, was that it would have been easy to take a knee-jerk reaction to sell a huge part of portfolios and raise a lot of cash.

"But in both cases, we have seen this would have been the wrong thing to do.

"Therefore, advisers keeping their clients on the right journey will continue to be an important part of their work in 2018 and in the years to come."

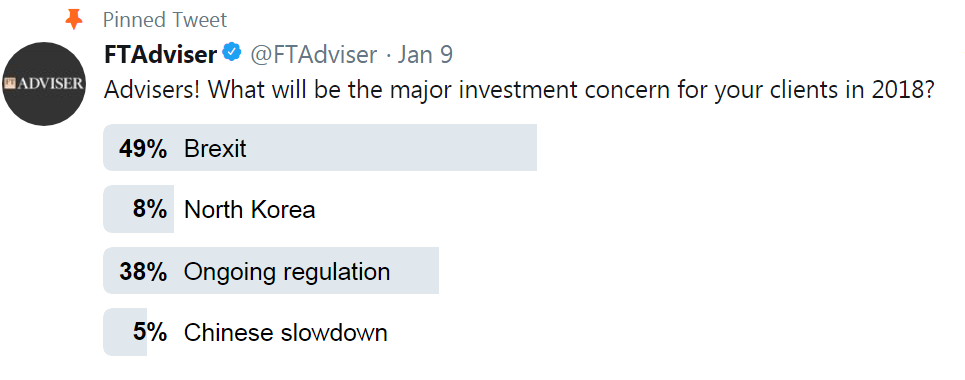

Twin fears for advisers in 2018

Brexit and ongoing regulatory activity are posing two threats to clients' portfolios over the coming year, advisers have claimed.

In the light of failed UK companies such as Carrillion struggling to compensate for the loss of large-scale contracts - which some analysts have put down to Brexit - advisers have claimed uncertainty over the terms of the UK's departure from Europe is a big concern.

In a poll among financial advisers, 49 per cent cited Brexit as the biggest concern for 2018 and 38 per cent said ongoing regulation would pose potential problems over the course of the year.

Commenting on FTAdviser Talking Point's poll, property investment adviser Proactive Consult stated: "There are loads of regulations coming up and we have already seen many through. However, who knows which ones are in the pipeline?"

Despite concerns, some fund managers and wealth advisers believe the initial shock effects of Brexit, such as the fall in sterling and the subsequent rise in inflation, will dissipate over the course of the year.

David Hillier, portfolio manager in the multi-asset strategy group at Insight Investment, part of BNY Mellon, said: "In the UK, consumer and producer price data should show a continued decline in rates of inflation – in part as the impact of a weak pound post the Brexit decision unwinds."

Oliver Wallin, investment director at Octopus, also expressed positivity after three "key sticking-points" were resolved in terms of getting Brexit-ready.

He said: "Brexit negotiations moved on with the three key sticking points seemingly being resolved: the divorce settlement bill, rights of European Union citizens and the Irish border.

"Discussions can now move onto trade and discussions about the type of agreement the UK wants. There was talk of a transition period, which will be welcomed by business, and would take some of the time pressure off. All eyes will be on the next round of negotiations."

When a market correction comes, it will be sudden and savage as real fear returns

The concerns came as the FTSE 100 maintained its strong run, up 5.86 per cent year-on-year as of 15 January, with few signs of this abating, even given the bad news over construction companies.

Russ Mould, investment director at AJ Bell, said: "No signals look to be flashing danger – if anything all are flashing green for go.

"However, after what is now almost a nine-year bull run in UK stocks, this could be a reminder of Warren Buffett’s aphorism the right time to be fearful is when everyone is greedy and the right time to be greedy is when everyone is fearful, and right now there is little, if any, fear in evidence."

Guy Stephens, technical investment director for Rowan Dartington, said no matter what the fears: "For the time being, investors are remaining invested, mainly in equities and bonds, because there are few available alternatives.

"While there are no dark clouds with respect to earnings on the horizon, everyone is prepared to ignore the valuation concerns and keep their fingers crossed.

"When a market correction comes, it will be sudden and savage as real fear returns. Any investor who is not prepared to remain invested for the longer term and needs to crystallise value within the next couple of years should be careful indeed and consider a staggered programme of crystallisation rather than continue to ride the wave in anticipation of perfect timing.

"Arguably, the longer the bull market runs, the more savage the shock when it ends."

simoney.kyriakou@ft.com

CPD: What should we expect in 2018?

Words: Simoney Kyriakou. Images: Pexels

What should investors expect in 2018?

The start of a new year always brings with it a sense of hope and new direction, but what sort of trends might we see in the investment world?

Global markets started the year strongly. A slight dip on 2 January from the last day of trading on 29 December saw the FTSE 100 breathe slightly before rising steadily to an all-time high of 7792.56.

The S&P 500 has been nudging 2,802.56 over January, President Donald Trump has been tweeting about the record highs on the Dow Jones, the Nikkei 225 has been edging above 23,700 and even up to 24,000, and the strong performance seen on the Dax in the second half of 2017 seems to be continuing into 2018. So far, so good.

Over 2017 market dividends have also been strong, despite commentators talking of ‘compression’ on equity income yields. With 4.2 per cent currently on the FTSE 100, above 3 per cent inflation, investors are still seemingly being compensated in both growth and yield.

And despite inflation creeping up, and fixed income yields remaining tight - especially in developed economies - there are still advocates of higher-yield and selected corporate bonds.

But can the good times continue to roll?

Presaging the downturn

Donald Maxwell-Scott, technical investment manager at Rowan Dartington, questions whether another financial crash is looming.

“The saying goes that the bull goes up the stairs and the bear falls out of the window. Global markets have continued to rise steadily; it seems there is nothing on the horizon to temper them, or is there?”

Although the markets have been on an impressive run, Mr Maxwell-Scott says there is “no shortage of market commentators predicting we are moments away from the end and financial doom awaits us all”.

But while they are warning about the crash, they are not predicting reasons why it might happen – and without any consensus on what might cause it, together with overweening government interference, quantitative easing (QE) and rising household debt, he feels there may not be one be-all, visible contributory factor to a crash.

For this reason, it is very hard to forecast when and whether and how deep a potential crash might be.

Gloomily, he presages: “We wouldn’t be so foolish as to predict when the next financial calamity will strike or what will be the cause, but with the amount of stimulus and action by governments it is unlikely to be one factor, but rather several different ones.”

Green for go in the UK?

Forecasts for the UK do not look great, if figures from the Organisation of Economic Co-operation and Development, as well as the UK's Office for Budget Responsibility, are anything to go by.

For example, the UK is forecast to see one of the lowest rates of growth in the G20 over the next 12 months in GDP (1.6 per cent) and corporate earnings (6.5 per cent), as a result of a tapped-out consumer and diminishing investment flows.

With uncertainty around Brexit and fears over continued capital flows into the UK, some fund managers and wealth managers are feeling less positive about the ability of UK equities and bonds to power through these political problems and emerge successful.

Chris Godding, chief investment officer of wealth management group Tilney, comments: “We have been reducing exposure to UK assets as we are wary of markets that become highly sensitive to political developments.”

There might be a correction or two, but for Russ Mould, investment director at AJ Bell, the five key danger signals are just not “flashing danger” when it comes to UK equities in 2018.

This quintuplet of possible danger comprises:

1) Transportation

2) Copper prices

3) Small-cap companies

4) Volatility

5) Valuations and the dividend yield.

But instead of copper prices trending down, small caps losing momentum, transportation stocks stalling, volatility peaking and valuations looking way too stretched - all of which would scream 'beware' - he finds the opposite is happening.

Take volatility. According to Mr Mould: “History shows stock indices progress best when they make serene progress and a series of modest gains, and tend to fare less well when trading is choppy and there are big swings up and down.

“The FTSE 100 moved higher with a minimum of fuss in 2017 when there were just 17 open-to-close movements of more than 1 per cent in the index throughout the whole year.

“That was the lowest total since 2005’s reading of 18 and the UK stockmarket advanced smartly for a further 18 months after that.

“Further peaceful gains, in incremental steps, would further encourage this is a bull run and not some frenzied bubble that is primed to burst, assuming historic trends repeat themselves.”

From a relative perspective, we believe the ECB is more likely to surprise the market than the Fed

In summary, he says these five signals are together still “flashing green for go”, even though we have had a nine-year bull run in UK stocks and what goes up surely must come down.

It just might not come down sharply in the near future, seems to be the message from these five indicators.

But what about the rest of the world? What of monetary policy, global fixed income, China and, of course, the US?

Monetary normality

Sterling started to show more strength at the beginning of 2018 as fears of a US government shutdown started to gain momentum.

This wasn’t a resounding show of support for the pound itself, but a sign of dollar weakness.

Miles Eakers, chief market analyst at Centtrip, comments on how sterling climbed to its highest level against the dollar, at 1.3932, in 18 months during January.

He says: “The fall [in the dollar] comes amid the looming possibility of a government shutdown as Republicans struggle to secure a stop-gap bill and Democrat leaders are blocking legislation to fund the government further until President Trump concedes ground on his immigration policy.

“While political turmoil has been taking its toll on USD, perhaps Trump’s tax plan may offer some hope of a recovery for the US currency?”

Eugene Philalithis, portfolio manager of the Fidelity Multi Asset Income fund, is pretty sanguine about the prospects for the dollar.

He explains: “While we do not expect a material appreciation in the dollar across 2018, we still expect it to strengthen across the year.

“The currency has been testing its lows from the past two years, but the strong economic backdrop should mean it avoids any further depreciation, especially after 2017’s meaningful correction.

“At the same time, currencies like the euro remain vulnerable to political risks, with Italian elections due to be held before May this year and ongoing uncertainty around Brexit and the make-up of a governing coalition in Germany.”

Mr Godding believes while currency moves are difficult to call, Tilney’s “base case at the moment is that sterling will remain cheap or weaken relative to the dollar and euro”.

Over the longer-term, some commentators believe the biggest currency surprises might be from Europe, rather than the US and the UK.

Enzo Puntillo, head of fixed income for GAM, states monetary policy at the European Central Bank (ECB) might be something for investors to watch this year.

He says: “From a relative perspective, we believe the ECB is more likely to surprise the market than the Fed.”

Europe

When it comes to fixed income, fiscal policy might have a role to play in how managers structure their bond portfolios in 2018.

For example, as a result of the ECB’s monetary policy, Mr Puntillo suggests there could be better performance seen in the US than in Europe.

He explains: “Given the fact that the European cyclical economic expansion is less mature than in the US, this would support a convergence of the spread between German and US 10-year bond yields, meaning German Bunds are likely to underperform against US Treasuries.

“This is a key theme we will be playing in our portfolios in 2018.”

Mr Maxwell-Scott adds: “QE has run into the trillions globally, and now the health of the global economy is seemingly improving, many central banks are reining in their programmes.

“The worry is that this feature, when coupled with increasing interest rates, could lead to a significant fall in bond markets.”

But Niall Gallagher, investment director for European equities at GAM, is more upbeat about Europe’s prospects.

Our own forecasts suggest continued strong growth for the rest of the world in 2018

He comments: “We have two key investment themes underpinning our stock selection process.

“On the one hand, we have exposure to long-term secular growth trends: emerging market consumption growth, transfer from the physical to the online world, and disruption of whole industries through new technology.

“On the other hand, our medium-term focus – the one with more potential to drive returns in 2018 – is our positive and above-consensus stance on European domestic demand.

“We are positioned to benefit from a eurozone demand recovery through select key holdings in building and construction materials, consumer spending and business investment.

“We believe the risk/reward profile is highly skewed to the upside, with a multi-year recovery potential.”

US outlook

If you follow President Trump on Twitter, barely a day goes by without positive-sounding tweets about the strength of the US equity market and the positive upswing across various sectors.

As of Wednesday 17 January, the Dow had closed with a gain of 31.7 per cent since President Trump’s inauguration date of 20 January 2017.

All eyes were on the industrials to see how it would fare by close on Friday 19 January, as the index was on course to have generated the best return ever in the first year of any post-war president.

“This is something which Donald Trump may well be keen to crow about on Twitter,” according to Mr Mould.

The following table shows the rise in stockmarkets in the first year of US presidential terms since 1949.

President Obama's first year in his first term has been the strongest so far at 33.4 per cent, but Mr Trump has been hot on his heels.

Source: AJBell/Thomson Reuters/Datastream

The S&P 500 has also gone from strength to strength.

The Faang stocks – Facebook, Apple, Amazon, Netflix and Google – have driven the large-cap markets ever-higher but how much bigger can these behemoths get?

Can they push price-earnings ratios even higher in 2018? And what sort of risks might a heavy skew towards social media companies pose for the index?

Tilney’s Mr Godding comments: “The strength of the global economy is a double edged sword for investors.

“Higher growth leads to higher corporate earnings and the rise in equities last year was principally driven by strong earnings growth.

“However, GDP growth can also lead to the real economy absorbing more of the excess liquidity in the system, via higher investment and working capital to effectively crowd out financial money flows.”

With lower tax rates to be implemented in the US this year, following a last-minute successful passage of a tax bill through congress and the senate in December 2017, Mr Godding says the tax rates should incentivise investment in capital assets.

He adds: “US equity returns this year should broadly reflect the circa 12 per cent earnings growth currently factored in by the markets.”

Japan

While Japanese 10-year government bonds are still sitting at 0 per cent, there doesn’t seem to be a thriving fixed income market, but for equity investors the prospects for 2018 might be a little more rosy.

According to Ernst Glanzmann, portfolio manager for Japanese equities at GAM, there are significant strides being made in automation and robotics, which is helping to fuel better efficiency in terms of labour and employment.

He says: “One of the top themes for Japan in 2018 will be more work process improvement due to an ever tighter labour market.

“Companies will be eager to contain cost pressure as much as possible. One way of doing this is by further standardising processes through the application of IT-based solutions –automation, robotics, artificial intelligence and the internet of things.”

China

Few investors will forget the beginning of 2016 when Chinese growth slowed down so much global indices trembled.

But over 2017, Chinese GDP surprised on the upside, with 6.8 per cent annual growth, a recovery in industrial production and fixed asset investment, with stronger exports, up 8.8 per cent on 2017.

We believe we will continue to see increasing focus and effort from asset owners on improving investee companies’ carbon risk management and disclosures

According to some commentators, Chinese consumers are going to be a strong trend, as the country undergoes its economic evolution to a consumer-driven economy.

Luxury companies in the consumer, technology, healthcare and financial services sectors are continuing to experience strong growth, although overall retail sales growth was slightly lower at 10.2 per cent compared with 10.4 per cent in 2016.

But has China’s growth story peaked? Craig Botham, emerging markets economist for Schroders, believes there is resilience and strength in the country for investors in 2018.

Mr Botham explains: “The data paints a picture of an economy supported by a strong external backdrop.

“Our own forecasts suggest continued strong growth for the rest of the world in 2018, so the export sector should continue to provide support for the economy, even if an acceleration is unlikely.”

Other themes for 2018

There are other themes to watch out for this year, as certain demographic groups emerge and disruptive technologies drive change.

GAM’s Scilla Huang Sun, portfolio manager for luxury equities, says the team’s “big theme” for 2018 is: “What do millennials really want?

“Millennials are increasingly becoming the main target group for most luxury companies.”

Then there is the rising green economy. Lisa Beauvilain, head of sustainability and ESG at Impax, says: “Carbon risk in investment portfolios is becoming widely acknowledged.

“We believe we will continue to see increasing focus and effort from asset owners on improving investee companies’ carbon risk management and disclosures following the Task Force for Financial Disclosure (TCFD) recommendations that were launched in 2017.”

She believes investors are also likely to be highly focused this year on the risks and opportunities stemming from issues such as single-use plastics and packaging, as well as cybersecurity.

Ms Beauvilain adds: “Mapping the sustainable development goals (SDGs) to investments and companies looks set to continue in 2018, but we believe these need to be assessed and reported with improved intentionality and rigour.”

Conclusion

There are reasons for concern as equity markets stretch higher, fiscal intervention by governments starts to loosen and bond yields remain contracted.

Wariness, rather than unabated enthusiasm (such as we have seen in the recent crypto-currency frenzy) should be the watchword this year.

But even in sectors where there has already been years of strong growth, fund managers believe there will be opportunities for canny investors.

Moreover, new growth markets are starting to emerge in clean energy, technology and luxury retailing, suggesting there are some interesting pockets of promise for investors to consider over the course of 2018.

Simoney Kyriakou is content plus editor for FTAdviser

The house view from Peter Harrison, group chief executive of Schroders

As investors look ahead to a new year, they could be forgiven for wondering whether they will be as pleasantly surprised in 2018 as they were in 2017.

A number of political worries on the horizon this time last year signally failed to materialise, including the likely shape of President Trump’s trade policies, the rise of populism in Europe and fears over North Korea.

As it turned out, the market shrugged all these aside, with both interest rates and market volatility remaining close to historic lows, while stockmarkets hit new highs.

Nearly a year on, the same worries remain, compounded by the question of how markets will react to the gradual withdrawal of quantitative easing (QE).

Investors may well ask whether these problems have been deferred or whether markets will again take them in their stride. We have gathered together the collective wisdom of our investment teams on these questions.

A number of themes emerge:

1) Valuations are stretched nearly everywhere, underpinned by low inflation and minimal interest rates. Japan stands out as one of the few attractively valued equity markets. In both Japan and Europe, stock prices should benefit from expanding profit margins which have room to catch up with other parts of the world.

2) While both inflation and interest rates should rise in 2018, few foresee them getting out of hand. However, several of our investors suggest that the market consensus is too sanguine about inflation.

The main risk we see lies in reflation, as governments turn to lower taxes and higher infrastructure spending to stimulate economies

3) One area of the equity market likely to stand out is value (cheaply-valued stocks). After the longest period of underperformance in over 40 years, the catalyst for a turnaround could be a rise in inflation and therefore interest rates.

4) Assuming policymakers can successfully juggle sustaining the recovery with controlling inflation, global bonds should not experience much downside. A keen eye will need to be kept on inflation, though.

5) In emerging markets, attractive yields for both dollar and local currency debt should be supported by continuing strong growth and relatively low inflation, alongside a stable dollar. Investors still need to beware of political developments though.

Overall, we carry a spirit of cautious optimism into 2018

In China, valuations look stretched, while growth may slow, dragged by debt reduction, particularly in the property market, and rising raw material costs, which may squeeze margins. However, domestic consumption and investment should hold firm, with selected sectors growing earnings.

6) The overall background should be good for active managers, given a likely pick-up in both volatility and dispersion (the differences between individual stock returns), alongside a fall in correlations (the extent to which stocks move together).

7) The challenges of managing businesses sustainably continue to grow, including the globalisation of policy, the increasing costs of misjudging technology and the ever-present background of climate change. Addressing them successfully will require an active approach.

If our forecasts prove accurate, GDP growth of 3.3 per cennt in 2018 will mark the strongest period for the global economy since 2011.

More important will be whether policymakers can maintain the “Goldilocks” combination of strong growth and low inflation as QE is withdrawn in the US and Europe.

The main risk we see lies in reflation, as governments turn to lower taxes and higher infrastructure spending to stimulate economies, which could lead to overheating and unexpected rises in inflation and interest rates.

Overall, we carry a spirit of cautious optimism into 2018, albeit that caution may start to overwhelm optimism as the year wears on.

It is certainly an approach we are adopting in our multi-asset portfolios, which go into 2018 with a pro-cyclical tilt in favour of equities, but with a readiness to ratchet down risk should circumstances demand it.